The 2024 ZipRecruiter Annual Employer Survey

What’s Next for the Labor Market

What’s on the horizon for the U.S. labor market? ZipRecruiter’s 2024 Annual Employer Survey offers exclusive insights from 2,000 hiring managers and talent acquisition professionals surveyed between September 24 and October 16, 2024.

The findings reveal a labor market at a crossroads: turnover rates are unusually low, hybrid work has cemented itself as the dominant model, wages are climbing, and hiring optimism is high. Yet beneath the surface, stark divides remain across industries and between organizations large and small.

From Churn to Stability: How Employers Perceive “The Great Stay”

ZipRecruiter finds a sharp decline in employee turnover from the previous year at surveyed businesses—the hallmark of what some are calling the “Great Stay.” Businesses reported an average annual turnover rate of 215% in 2023—meaning the typical firm replaced its entire workforce more than twice in a single year. In 2024, that figure dropped 37%, to 135%, marking a significant stabilization in workforce dynamics.

Smaller businesses saw the most dramatic improvements, with turnover rates falling over 60% on average among firms with fewer than 100 employees. Larger companies, while also experiencing improvements, recorded more modest declines, including a 12% reduction among firms with over 5,000 employees. This difference likely stems from smaller firms being hit hardest during the Great Resignation due to limited resources for competitive pay and benefits, and now having the greatest room to recover.

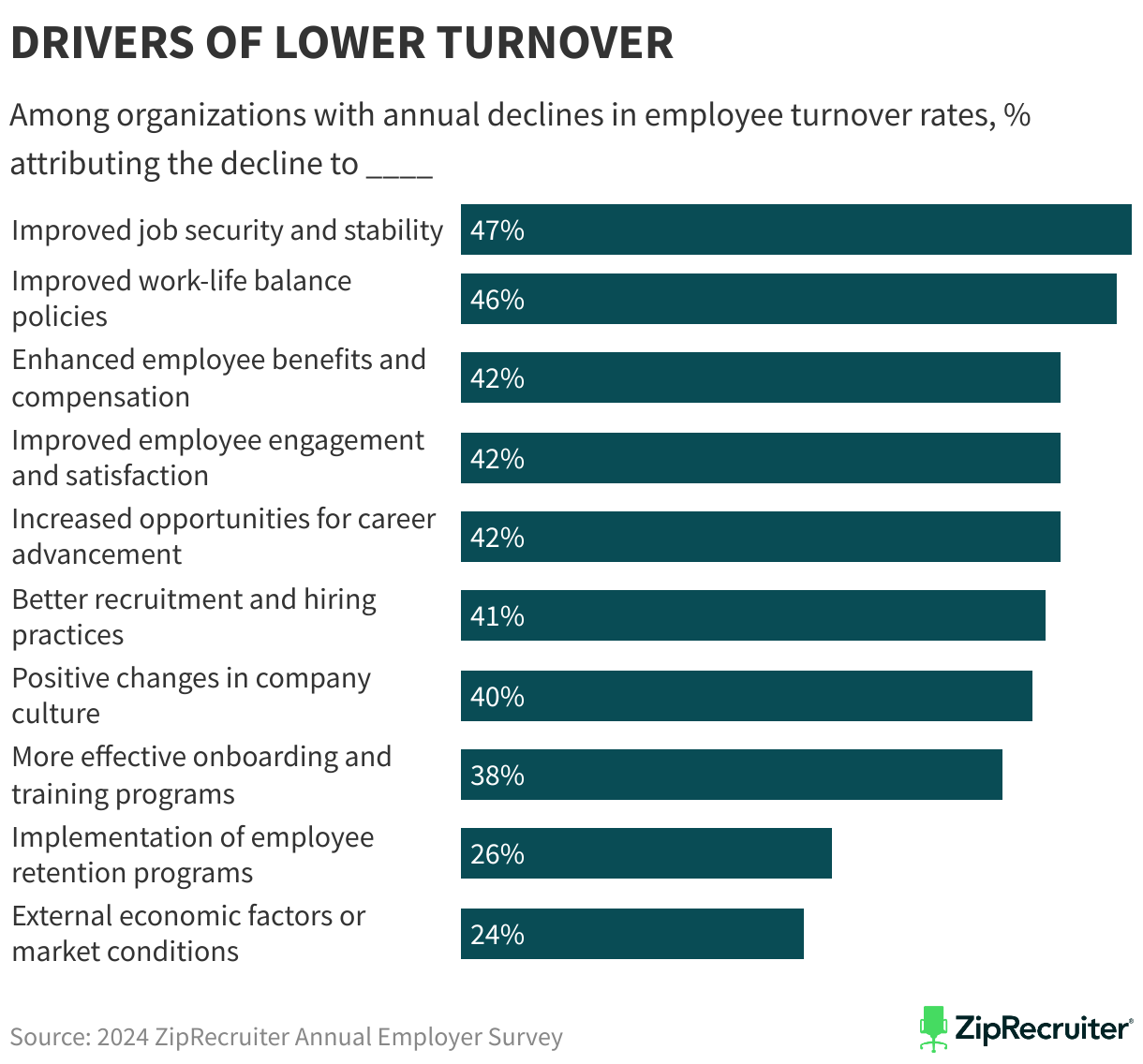

What’s Driving Lower Turnover?

While a steep decline in the so-called quits rate (the share of employed Americans leaving their jobs, mostly for other jobs) is a macroeconomic trend, most businesses attribute the drop in turnover in their own workforce to internal improvements rather than external conditions. Nearly half (47%) of companies with reduced attrition credited enhanced job security and stability, while 46% pointed to better work-life balance policies. Improvements in employee benefits and compensation packages, increased opportunities for career development, and efforts to boost employee engagement and satisfaction were each cited by about 42% of respondents. Other commonly credited strategies included better recruitment and hiring practices (41%), changes to company culture (40%), more effective onboarding and training programs (38%), and the implementation of formal employee retention programs (26%). In response to a separate question about compensation changes, 16% of respondents said their companies introduced retention or longevity bonuses in the past year, whereas only 4% removed them. External economic conditions, such as fewer opportunities for workers to jump ship, were cited by just 24% of employers.

In theory, one might expect turnover to decline if staying at the company becomes relatively more attractive with improved employment conditions, or if external employment opportunities become less attractive, or both. Our survey finds that companies have largely taken ownership of their retention success. However, this may reflect a cognitive bias, with employers overestimating the impact of their internal efforts and underestimating the role of external market conditions. If the macroeconomic environment improves and outside opportunities become more attractive, attrition could rebound despite these internal investments, potentially blindsiding companies that have grown accustomed to lower turnover.

Persistent Challenges in High-Turnover Firms

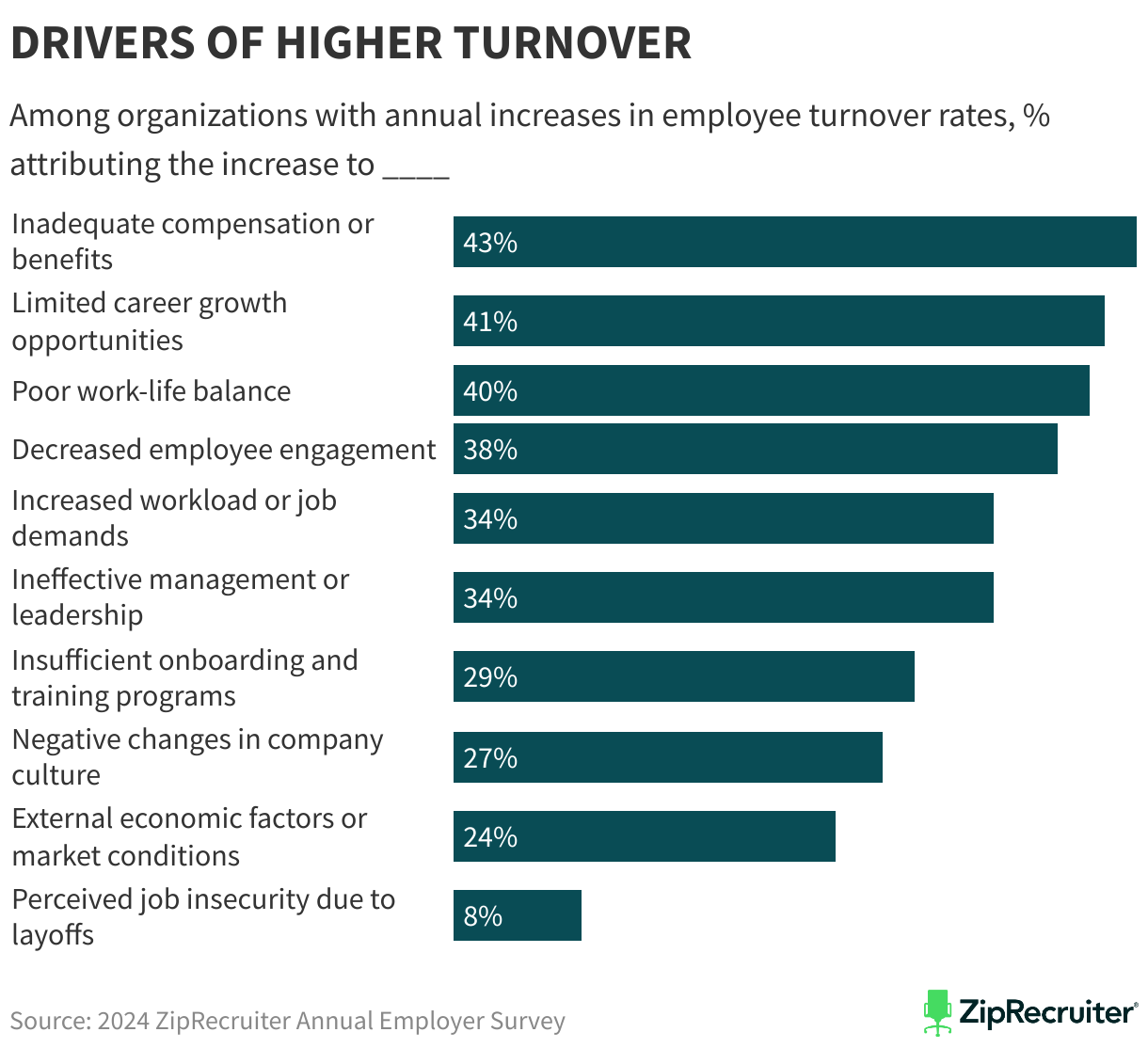

Not all employers shared in the gains. Nearly four-in-ten respondents (39%) said that they thought turnover had risen in their organizations in 2024. The most commonly cited factors were inadequate compensation or benefits (43%), limited career growth opportunities (41%), and poor work-life balance (40%). Decreased employee engagement (38%) and increased workloads (34%) also featured prominently, alongside issues such as ineffective management (34%) and insufficient onboarding and training programs (29%). Notably, 27% of surveyed companies reported negative changes in company culture over the past year.

Once again, a minority (24%) blamed external economic factors such as improved job opportunities within their industry. Layoffs and restructuring, often a key driver of attrition in past years, were less significant, with only 8% citing job insecurity as a factor.

Sector-Level Trends

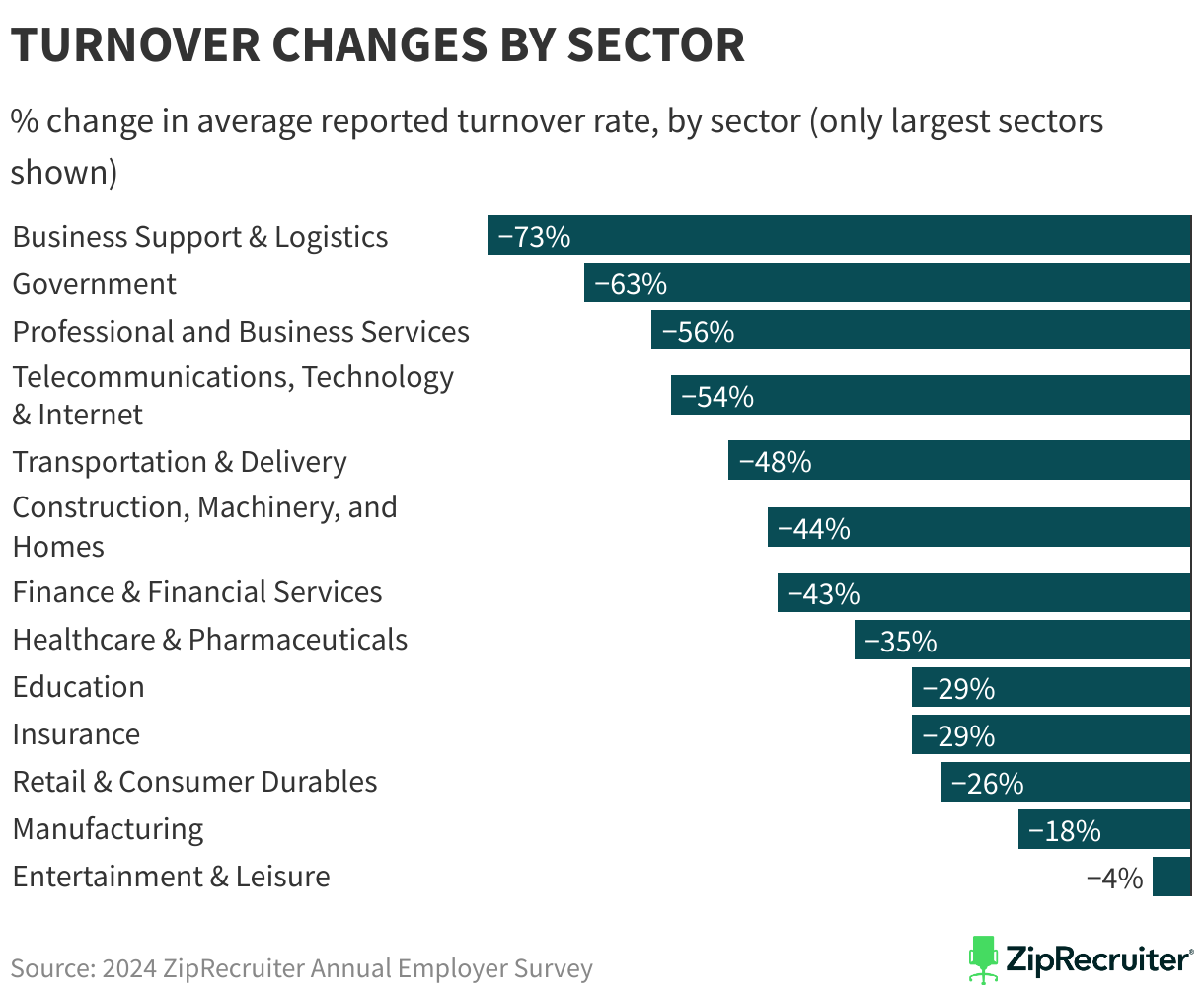

Declines in average reported turnover rates between the 2023 and 2024 surveys were uneven across industries. Business Support & Logistics saw the largest drop, with turnover falling 73%, followed by Government (-63%) and Professional and Business Services (-56%). In contrast, Manufacturing (-18%) and Entertainment & Leisure (-4%) recorded only modest declines.

The industry patterns suggest that churn can fall both in sectors with strong labor markets, such as the public sector, and in those with relatively weak markets, such as business services. After a period during the pandemic in which private sector wage growth was outpacing that in the public sector, public sector wage growth began to catch up in 2024. Job growth in the public sector also remained unusually strong. So declining turnover could reflect the relative improvement in public sector employment opportunities. On the other hand, turnover may have declined in business support services because employment in the sector has been on the decline and workers lucky enough to have jobs are sheltering in place.

A Return to Stability

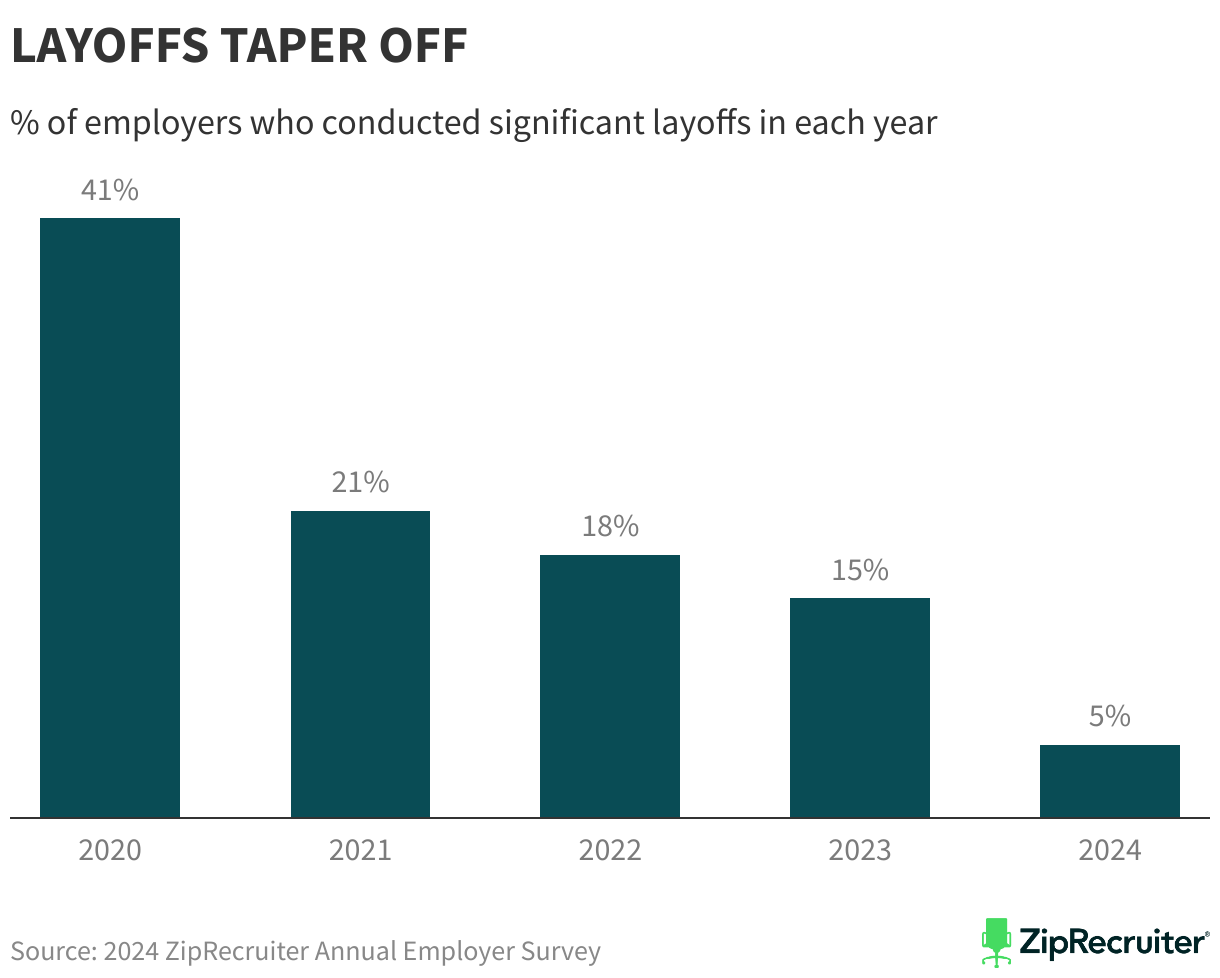

The turbulence of the pandemic-era labor market is increasingly in the rearview mirror. Major layoffs, which peaked in 2020 when 41% of surveyed firms reported significant reductions, have fallen steadily, dropping to just 5% in 2024. The result is a labor market characterized by greater predictability and stability, as businesses focus on retention and workforce planning rather than crisis management.

As the “Great Stay” unfolds, firms appear to be clinging to the lessons of the Great Resignation, investing in better compensation, work-life balance, and career development to hold onto talent. While challenges remain in some sectors—and while difficulties could easily crop up again in a tighter labor market—the overall trend suggests that we could continue to see relatively stable labor markets in the coming year.

Remote Work in 2024:

Companies Shift Toward Hybrid Models and Stricter Oversight

The evolution of remote work took a new turn in 2024, with companies refining their strategies to balance flexibility with structure. ZipRecruiter’s Second Annual Employer Survey reveals that hybrid work has solidified as the dominant model, but stricter in-office requirements and tighter compliance monitoring signal a shift away from the leniency of earlier pandemic years. At the same time, remote hiring is on the rise, driven by the promise of broader talent pools.

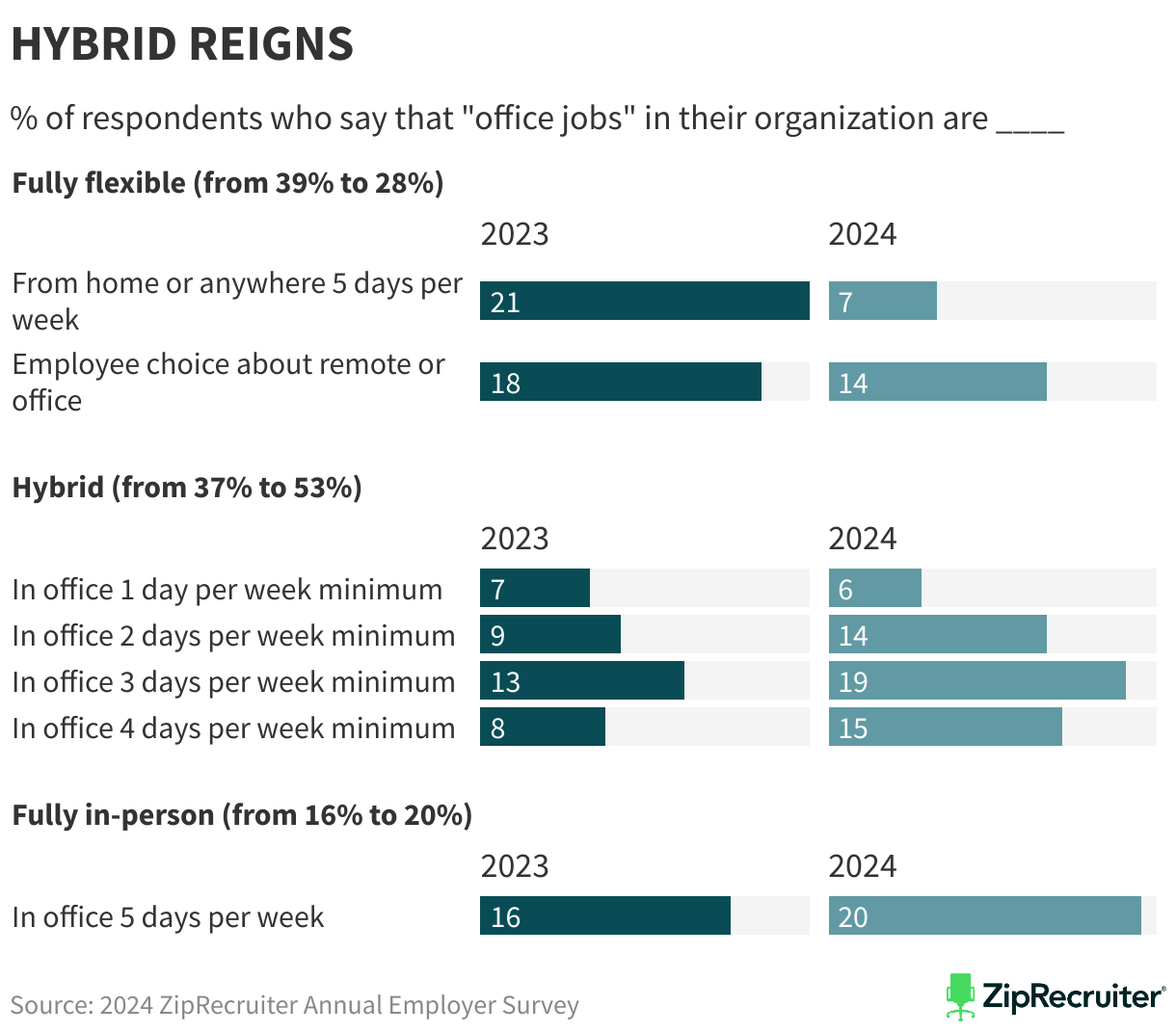

Hybrid Work Anchors the Workforce, Fully Remote Declines

Hybrid work remains the most common arrangement, with 40% of companies supporting a mix of in-office and remote work in 2024. Fully remote work, however, saw a sharp decline: only 7% of companies allowed workers in office jobs to be fully remote, compared to 21% in 2023. Similarly, the share of companies granting employees complete choice about working remotely or in-office fell from 18% to 14%.

Conversely, more organizations are requiring structured in-office attendance. The share of companies mandating employees to work in-office at least three days per week rose from 37% in 2023 to 53% in 2024. Full-time, five-day office attendance increased, climbing from 16% to 20%. This shift underscores a growing emphasis on consistency and predictability in how teams operate.

Overall Trends Mask Significant Polarization and Divergence

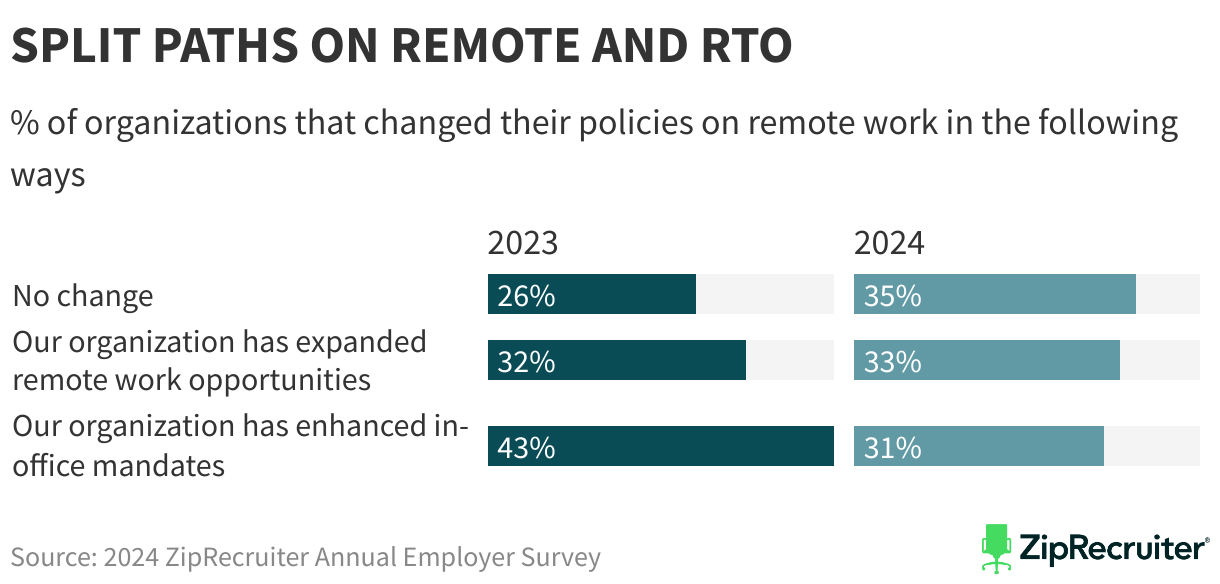

While some companies are pulling back remote opportunities, others are doubling down. In 2024, 31% of respondents said their companies reduced remote work opportunities, down from 43% in 2023. Meanwhile, 33% said they expanded remote work opportunities, a slight increase from 32% the year prior. These opposing trends indicate that companies are no longer taking a one-size-fits-all approach; instead, they are tailoring policies to their unique organizational needs.

Compliance monitoring has also grown stricter. Among companies with in-office requirements, 72% now monitor attendance, up from 64% in 2023. However, many still offer flexibility: 68% of companies allow employees to choose their in-office days, though this is slightly down from 72% in 2023.

Remote Hiring Expands but Becomes More Strategic

After years of adaptation during the pandemic, companies are increasingly hiring workers who are remote from the outset. The share of organizations actively recruiting remote workers rose from 16% in 2023 to 22% in 2024. By hiring beyond their geographic locations, companies are accessing a wider talent pool, especially in the tech sector, which saw the largest increases in remote recruitment.

This shift however comes with challenges. Employers are increasingly screening for traits associated with remote work success, such as self-motivation, communication skills, and the ability to work independently. These considerations also have pay implications: 12% of companies widened or introduced geographic pay differentials in the past year, while only 8% narrowed or removed them.

Culture and Productivity Concerns Still Shape the Debate

Cultural and productivity concerns remain key reasons why some organizations are pulling back on remote work. Among companies reducing remote opportunities, 59% cited concerns that remote work harms company culture, up from 53% in 2023. Productivity concerns, though still relevant, are diminishing. Among those companies cutting back on remote work, those citing manager perceptions of lower remote productivity fell from 61% to 57%, and those with some direct evidence dropped from 47% to 43%. These trends suggest that while fears about remote work persist, they may be rooted more in perception than data.

RTO Mandates: A Hidden Tool for Workforce Reduction?

The push for return-to-office (RTO) mandates may be more than a cultural or productivity-driven decision—it could also serve as a covert strategy for headcount reduction. Survey data reveals that companies expecting to cut hiring significantly are more likely to impose RTO mandates than to expand remote work opportunities (38% vs. 13%). Conversely, expanding remote work appears correlated with stronger growth: 82% of companies that have broadened remote work opportunities expect to increase hiring, compared to 76% of those scaling it back.

Companies that have imposed RTO mandates report annual turnover rates roughly 13% higher than those that have become more supportive of remote work (169% vs. 149%). They are also more than twice as likely to say that turnover has increased rather than decreased over the past year (51% vs. 24%). The differential is much smaller for companies that have leaned into remote work at (42% vs. 36%).

These findings suggest that RTO policies, while often framed as efforts to boost collaboration or efficiency, might in some cases function as a lever to encourage attrition and reduce workforce size without formal layoffs.

Industries Show Diverging Approaches

Different industries are responding to the evolving landscape of remote work in distinct ways. Surveyed organizations in sectors such as finance (+11 points), aerospace (+13 points), and nonprofits (+13 points) reported more fully remote roles than in 2023, while those in transportation (-10 points) and entertainment (-2 points) were less likely to report allowing remote work. In-office requirements also varied, with manufacturing (-31 points), logistics (-26 points), and construction (-25 points) leading reductions in five-day mandates, while government (+3 points) and utilities (+6 points) increased them.

The Bottom Line: A Workforce in Transition

The 2024 data underscores a labor market in flux. Hybrid work is firmly entrenched, but companies are increasingly prioritizing structure and oversight. Remote hiring is growing, but with it comes new challenges around screening, productivity, and pay equity. The push for flexibility remains strong, but the full-time office workweek is quietly regaining ground in some corners.

The State of Pay: Pay Set to Climb in 2025

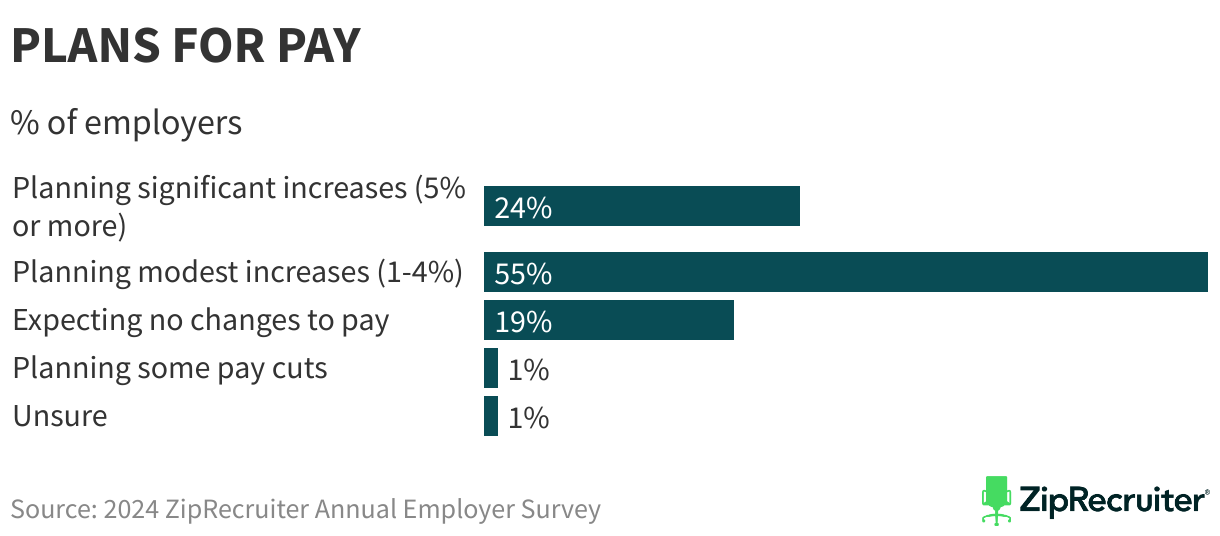

Employers are preparing for a stronger year in 2025, with the vast majority expecting to increase pay for workers. According to ZipRecruiter’s 2024 Employer Survey, 55% of employers plan modest pay increases of 1 to 4%, while 24% anticipate more substantial raises of 5% or more. This marks a sharp turnaround from the 2023 survey, when nearly half of employers (48%) reported resetting pay downward for certain roles amid fears of a recession.

How Employers Are Reshaping Compensation

The survey also reveals how employers have adjusted their pay structures over the past year to adapt to a dynamic labor market. Nearly half (41%) reported increasing base salaries for new hires, while a third (32%) introduced new pay scales or job tiers, and 30% increased the share of compensation tied to performance. Many are also using targeted incentives: 23% raised commission rates, 16% introduced retention or longevity bonuses, and 15% added opportunities to earn equity, such as stocks or RSUs. But not all adjustments have been upward. Some employers continued to cut costs, with 14% reducing base salaries for new hires, 13% freezing pay for existing employees, and 12% scaling back performance-based compensation. These changes, while less common, reflect lingering pressures in sectors like insurance and utilities, where a small but notable share of employers expect pay cuts to continue in 2025.

Where Pay Is Poised to Rise Most

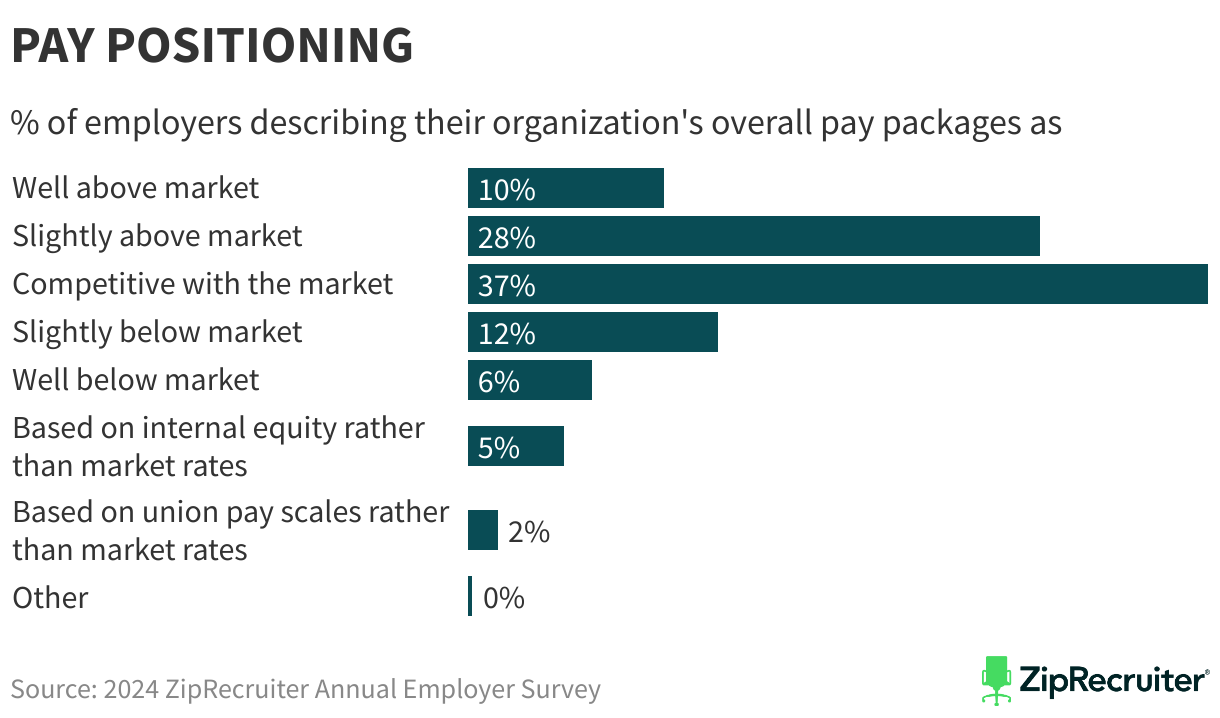

Larger companies are significantly more likely than smaller ones to plan major pay increases. For example, 30% of organizations with 5,000 or more employees plan pay increases of 5% or more, compared with just 13% of organizations with 10-49 employees. By industry, real estate, tech, and financial services stand out as the sectors where big raises are most likely in 2025. These industries, which have faced sluggish pay growth since the pandemic, could see a rebound as Federal Reserve rate cuts stimulate activity and boost business confidence.

Insurance and utilities are the only sectors where more than 5% of surveyed employers anticipate pay cuts, underscoring ongoing challenges in those areas. Overall, the data points to a labor market on firmer footing, with wage growth for new hires accelerating and employers across industries gearing up to compete for talent in the year ahead.

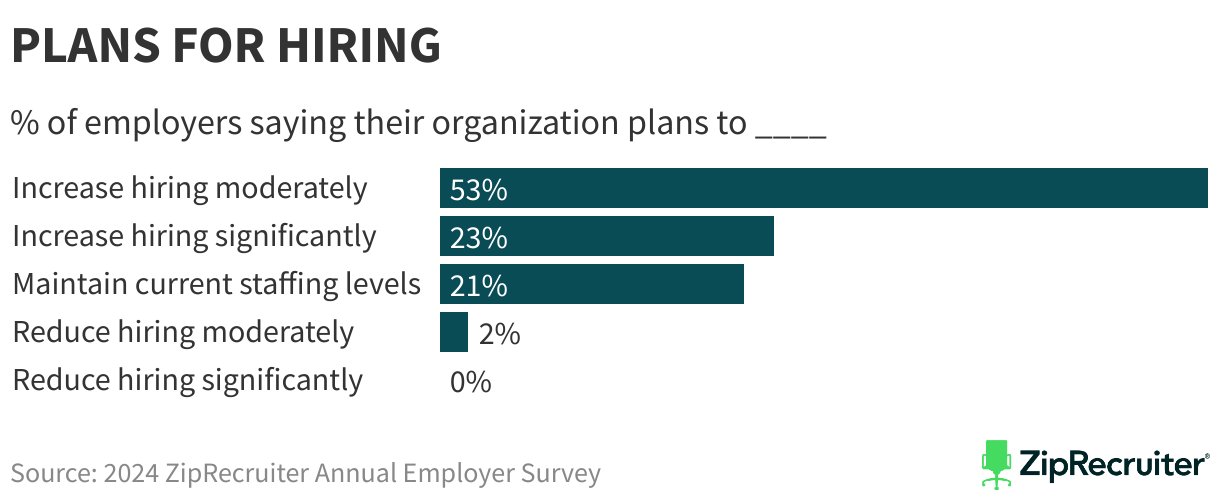

What the Labor Market Holds in 2025

A majority of U.S. employers expect hiring to pick up in 2025, signaling renewed optimism for the labor market after a year of slowing growth. According to ZipRecruiter’s Second Annual Employer Survey, 76% of employers say they plan to expand headcount in the coming year, with 53% anticipating modest increases and 23% expecting more significant growth. Meanwhile, 21% expect hiring to remain steady, and fewer than 4% predict workforce reductions.

This optimistic outlook follows a year in which the hiring rate steadily declined, reflecting a cooling labor market and reduced turnover. By August 2024, monthly hires had fallen to 3.3% of total employment—the slowest pace in 11 years outside the pandemic recession. For context, the hiring rate averaged 3.9% in the two years preceding the pandemic.

Industries Leading the Charge

The hiring outlook is strongest in industries tied to innovation and rising demand. Employers in technology (84%), insurance (82%), manufacturing (81%), financial services (80%), and healthcare (79%) are the most likely to expect an increase in hiring. By contrast, optimism is more tempered—but still positive—in sectors including government (65%), transportation and warehousing (63%), advertising and marketing (58%), the nonprofit sector (58%), and airlines and aerospace (58%). Larger businesses are more likely than smaller ones to anticipate headcount growth.

What’s Driving Optimism?

Employers’ hiring plans reflect the influence of macroeconomic conditions, technological advancements, and industry-specific trends, with more companies expecting these factors to drive growth rather than reductions. Nearly two-thirds (64%) of employers say macroeconomic factors like easing inflation, stabilizing interest rates, and a steady unemployment rate, are likely to support headcount growth in 2025, compared to 36% who expect macroeconomic forces to drive cuts.

Similarly, 59% of companies see technological advancements—such as artificial intelligence and digitalization—as a driver of hiring, though 41% warn that automation and efficiency gains could lead to reductions. Industry-specific trends are the strongest catalyst for optimism: 69% of employers cite rising demand in areas like lithium production, data center construction, and home healthcare as reasons to expand their workforce, with only 31% expecting industry-specific trends to force a pullback. This data suggests that while employers remain cautious about external risks, they see more opportunities than threats heading into the new year.

Survey Methodology

ZipRecruiter conducted a national online survey between September 24 and October 16, 2024, to explore employer attitudes toward recent hiring trends and their experiences of current U.S. labor market conditions. The survey was administered to a Qualtrics panel of 2,000+ verified talent acquisition professionals and hiring managers, each of whom has considerable responsibility for hiring processes and decisions. They were drawn from businesses of various sizes across a wide range of industries. In addition to standard screening and demographic questions, respondents were asked about their recruiting, hiring, employment, and retention practices, as well as their expectations, desires, and requirements for future talent acquisition activities.